Third Annual Survey of Pennsylvania Business Leaders

2/7/12

Summary of Findings

Summary

The Third Annual First Niagara Survey of Pennsylvania Business Leaders conducted by the Siena College Research Institute (SRI) shows that CEO confidence declined since last year but remains at a level where CEO’s express more optimism than pessimism towards economic conditions in Pennsylvania. Despite disappointment that 2011 failed to live up to their expectations, the vast majority lean towards 2012 being a better year and while revenue and profit projections are unchanged from last year, CEO’s plan to acquire fixed assets and enlarge their workforce at an increasing rate. While still critical, CEO’s have an improving assessment of state government’s efforts to create a successful business climate and nearly a third are at least somewhat confident that the state government will work to improve business conditions in 2012. Increasing numbers of CEO’s are now concentrating on growing their businesses and serving their clients more so than on cutting costs. Sentiment may have slipped due to a failure to meet expectations but more CEO’s have adjusted to the ‘New Normal’ and are cautiously growing their businesses. Based on Pennsylvania’s CEO’s, 2012 is likely to be a somewhat stronger year in the Keystone State.

Business Leader Confidence

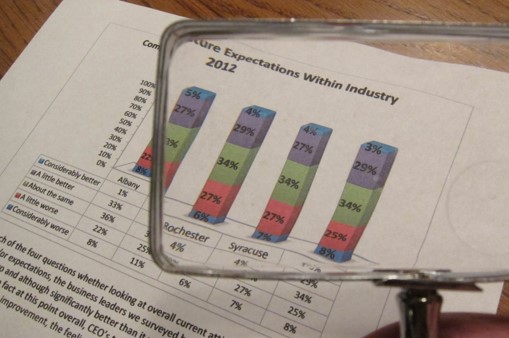

The overall Index of Pennsylvania Business Leaders slipped to 112.1 down 3.6 points from last year but it remains 12.5 points above two years ago. The Index continues to be well above the 100 mark, at which equal percentages of CEO’s are both optimistic and pessimistic about economic conditions in their industry and across the state. The current index component that assesses business conditions today as compared to six months earlier is now 104.7 virtually unchanged from last year but up 22.4 from 2009. The future component that measures expectations for the coming year is 119.5 down 7.7 from a year ago. Forty-two percent, down from 46 percent a year ago, of CEO’s of private, for-profit companies with sales between $5 million and $200 million in Philadelphia, Pittsburgh, as well as in Allentown, Altoona, Erie, Harrisburg, Lancaster, Reading, Scranton and York expect better economic conditions in Pennsylvania next year. Twenty percent, up from 17 percent a year ago, anticipate worsening conditions.

This survey reports data from 865 corporate leaders drawn from Service (23%), Manufacturing (20%), Retail (18%), Engineering/Construction (14%), Wholesale/Distribution (13%), Financial (6%) and Food/Beverage (6%). If equal numbers of CEO’s had positive and negative perceptions of and expectations for the general economy as well as for the condition of and future for their industry, the overall index would be 100. Food/Beverage (117.9), Manufacturing (116.1), Service (114.0), Retail (113.3) and Wholesale/Distribution (112.6) have the highest overall index readings but, aside from Service and Food/Beverage, all were down from last year.

Twenty-four percent of CEO’s say that business conditions have worsened in Pennsylvania over the last half of 2011 while 32 percent feel as though the economy has improved. Pennsylvania has settled in at a point where for two years slightly more CEO’s say conditions have already begun to improve rather than those that continue to experience decline. And looking to the future, by ratios that near two-to-one but at a rate less than last year, CEO’s anticipate ever improving economic conditions across the state and within their industry.

Based upon CEO’s responses to the four key index questions, the study identifies three distinct groups of business leaders today in Pennsylvania. Thirty-nine percent of CEO’s, down from 43 percent a year ago, report being able to currently thrive and are strongly optimistic about the future. Forty-four percent of CEO’s (up from 43% in 2010) acknowledge being seriously impacted by recent economic conditions and while they do not expect things to get worse, they do not anticipate improvement in 2012. The remaining 17 percent (up from 15% a year ago) have been very seriously affected by the economy and believe that economic conditions may continue to worsen in both Pennsylvania and their industry before getting better.

Revenues, Profits and Labor Force

Expectations for revenues and profits through 2012 are unchanged among CEO’s this year. CEO’s plans to acquire new fixed assets are up again this year and more than three times as many, 30 percent plan to enlarge their workforce this year as compared to 9 percent (down from 11%) planning layoffs.

Forty-six percent of CEO’s anticipate increasing revenues during 2012, and 20 percent up, from 17 percent last year, expect less revenue. Thirty-six percent anticipate increasing profitability this year (down from 37%) while only 25 percent (down from 26%), continue to expect profitability declines.

Despite declining confidence and stagnant expectations towards revenues and profits, fixed asset acquisition plans increased for the second consecutive year to 46 percent (up from 40% in 2009, 43% in 2010). Of those that do anticipate asset acquisitions, 54 percent plan to use internally generated funds as opposed to either borrowing from a financial institution (31% up from 27%) or private equity (6%).

Thirty percent of business leaders expect to at least moderately increase their workforce in 2012 up from 25 percent a year ago. While 61 percent intend to have their workforce remain the same, only 9 percent, down from 11 percent, plan on decreasing their labor force. Pennsylvania’s CEO’s while disappointed in not having had a better year and still leery of the future are investing in their fixed assets and workforce at an increasing rate.

Concentrations, Challenges and Attitudes towards Government

Today a growing number of CEO’s are becoming more focused on growing the market for their products and services and less focused on cutting costs. Market growth as a top profit enhancement strategy increased to 44 percent from 39 percent and cost reduction fell from 32 percent to 30 percent as the top profit enhancement strategy.

The top two concerns among Pennsylvania business leaders are, when asked to name their single most vexing problem, adverse economic conditions (22%) and governmental regulation (22%).

Thirty-six percent, an improvement from last year’s 50 percent, say the government of Pennsylvania has been doing a poor job of creating a business climate in which their company can succeed and 67 percent are either not very or not at all confident in the ability of the government to improve the business climate in Pennsylvania. As bad as that assessment is of state government, these CEO’s have an even more negative assessment of the federal government. Nearly three-quarters say D.C. is doing a poor job of creating a successful business climate. They strongly call for the development of domestic energy supplies, a balanced budget amendment, reducing corporate taxes, capping increases of federal regulatory spending increases at $0, repealing the health care reform legislation, and a temporary reduction in employer payroll taxes. A majority oppose an increase in taxes for those making over $250,000 a year and most oppose an extension of unemployment benefits.